I’m going to review the various options self-employed families have for healthcare in 2018 including one that is very intriguing. But, first, I’m excited to announce the winners of the “Guess Ken’s Premium Increase” contest!

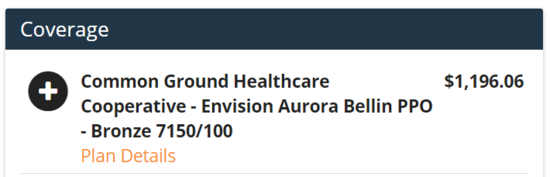

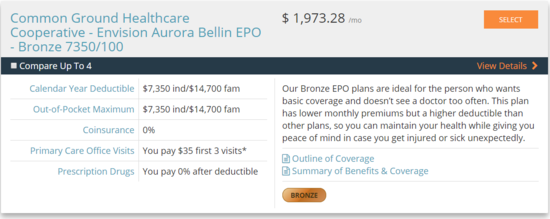

Guesses ranged from 12% to 147%. However, my family’s actual premium increase for the same plan in 2018 is 65%! That makes Nate Kern the winner with the closest guess of 51%. Screenshots below show 2017 and 2018 premiums.

Between premiums (~$24,000 for the year) and the family deductible ($14,700), our break even will be just about $39,000 in 2018. Think about that for a moment; even $24,000 in premiums still leaves our family on the hook for thousands of dollars. Unfortunately, this is not the first year of double digit increases for our family. Double-digit increases, eliminated plans and skyrocketing deductibles have been the norm for several years since the PPACA was first enacted.

Healthcare spending in the U.S. now accounts for almost 20% of GDP while it was just 5% of GDP in 1960! That leaves 15% less for buying other things and, more importantly, 15% less for saving and investment.

Random Drawing Winner

I only had five entries (four different people) for the random drawing. An entry was earned by sharing my post on Facebook or Twitter. The winner of the random drawing is….. Jon Goral! Congratulations, Jon!

Healthcare Options

So what now? What can my family, and other families, do about this? Let’s explore some options (hint: at this point I’m leaning towards option #7):

1. Bite the bullet and buy the insurance

- I can do this, but I’d hate to spend $24,000 for something that most likely won’t even cover our medical expenses. I’d basically be paying $24,000 for catastrophic coverage, which seems far too expensive for the coverage we’d be getting.

2. Go without insurance altogether and hope our family incurs less than $39,000 of medical expenses to break-even.

- More likely than not I would end up ahead in this scenario but would also have significant exposure if something catastrophic were to happen.

3. Go without insurance, but then, if a major medical issue arose in our family, get a job that offered health benefits.

- This is a pretty creative solution, but there’s neither a guarantee I could get a job on the spot nor would I want to take any time away from my business and my clients.

4. Look into “associating” with other small business owners and purchasing insurance as a group.

5. Suppress my income by increasing business expenses in 2018 so that our family could qualify for premium tax credits to offset the monthly premiums, but then I’d still be spending money I don’t need to spend.

6. Apply for an exemption to become eligible for a catastrophic plan. Although, even if I were approved, would premiums would be that much cheaper? After all, this Bronze plan already acts much like a catastrophic plan anyway.

7. Join a Health Cost Sharing Ministry (HCSM), which is a health sharing arrangement for people who share similar and strongly-held beliefs.

- Basically, the members pool together to aid and share in other members’ medical costs. This may be cheaper for a few reasons: (1) They can discriminate based on lifestyle so members tend to be healthier, which means lower medical costs and faster recoveries, (2) Pre-existing conditions are not covered the first year and are capped in years two and three, and (3) they may not have all the mandated coverages if a particular group finds certain procedures / coverage objectionable.

- Coverage from the pool kicks in after a family spends “X” dollars of their own money, much like a deductible. The one I’m considering as a $500 “deductible” per individual and $1,500 for the family while the monthly premium is only $449 / month with $1,000,000 coverage per incident! So this may save us about $18,000 of premiums and, if we have medical needs, thousands more dollars in out-of-pocket costs!

- Two common HCSMs are Liberty HealthShare and Christian Healthcare Ministries

One Reply to “Winners Announced and Healthcare Options for 2018 if You’re Self-Employed”

Comments are closed.